2026 Quarter One Update

Happy Spring and it has been quite a year so far!

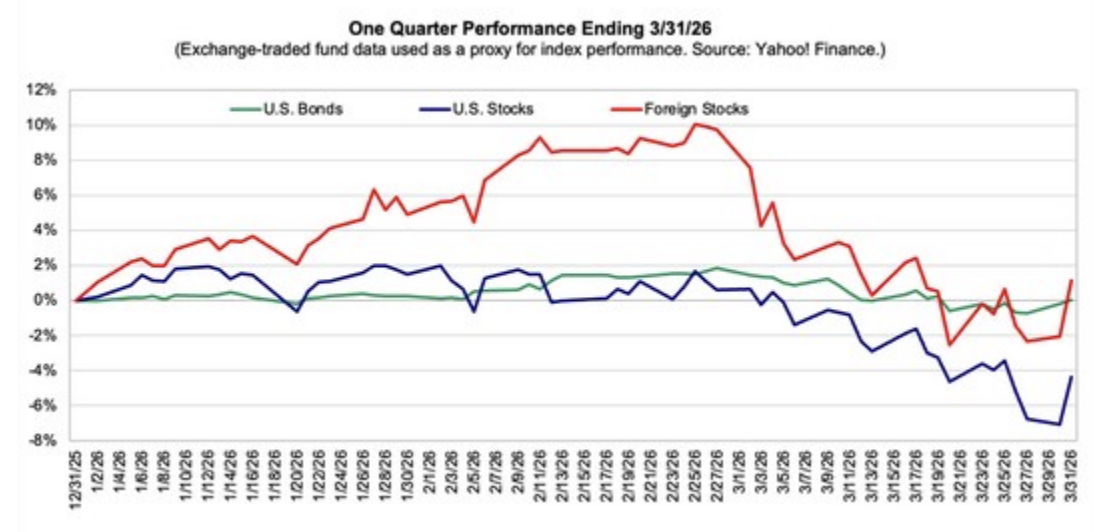

Stock and bond markets were off to a good start earlier in the quarter. Bond values rose as their yields edged down with folks pricing in several interest rate cuts going forward and as inflation expectations eased back a bit.

On the equity side of the ledger, stocks rose early in the quarter, buoyed by the prospect of positive economic growth and continued optimism about the potential for productivity growth from the broad deployment of AI.

The war in Iran has caused markets to sing a different tune of late. While wars themselves are not popular with investors due to the layers of uncertainty that they generate, this particular war has struck a painful nerve as Iran retaliated around the region, bombing the refineries and other facilities that so much of the world depends on to provide oil, natural gas, fertilizers and other energy feedstocks.

The loss of access to the energy products on which so many rely has affected economic and market predictions in many ways. Higher prices for energy items crowd out spending on other things. The price of oil ripples through the economy, as so many of the products and services we depend on become more expensive as energy costs mount.

This, in turn, fuels fear of higher inflation, slower economic growth, and the resultant possibility of potential recession. None of us, markets included, like the sound of any of that. Only time will tell how this all plays out, but for now we have a lot of uncertainty to navigate as the administration decides just how much longer they will engage in this conflict, and the Iranians decide how they will act regarding the Strait of Hormuz.

So far, even with the downturns in stocks and bonds, your diversified portfolios have held up well. Your large company equity allocations have benefited from a tilt toward more conservative, value-oriented holdings and away from the more richly valued technology and growth shares. A similar positioning in the shares of small and medium sized companies delivered a similar result.

International holdings as a group benefited mostly from the emerging markets allocation with the shares of countries involved in energy production and those producing memory chips profiting from strong demand. Developed market international holdings started strong and declined the most, as many of those countries look to be the most disadvantaged from the crimp in energy supplies from the middle east.

Your bond holdings ended the quarter down a bit, but not excessively so. Your holdings in floating rate bonds rode to the rescue again, as they are not generally affected by rising interest rates, the very item that caused the decline in most high-quality bonds.

We hope, as do so many others, that by the time we write to you next quarter the noise of war will have ceased in Iran. Our administration has indicated their preference for a quick close to this conflict, and we can believe them in this regard as the war and resultant higher domestic costs associated with it are deeply unpopular.

The jury is still out on the longer-term economic repercussions of the war. It is possible that higher energy prices could take their toll for some time longer. How that will affect our own economy as time marches on is still unknown, although we do remain optimistic. We have a lot going for us domestically and, should this wrap up somewhat soon, we do think that growth will continue to be the order of the day.

This year so far, with all its tumult and uncertainty, has been another reminder of why diversification is so important. Recession or no, diversified portfolios with attention paid to valuation continue to make the most sense for most investors. Trying to guess the future, except for those lucky few, is a fool’s game, and the subsequent attempt to time the market leaves most in worse shape than if they had stayed diversified and stayed invested.

At HFN, we value the opportunity to partner with you in strategies to build and preserve your financial future. With each quarterly update, we aim to provide a clear picture of market trends, your portfolio’s positioning, and the steps we’re taking together to help you stay on track toward your goals.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.